TOGETHER LET’S ACHIEVE SOMETHING INCREDIBLE

Education means dignity and life. Help build a future for children in rural India.

With each contribution, no matter big or small, you help a child reach closer to education. This enables him/her to provide a better life to his family such that each child educated is each family helped. These children are equipped with knowledge and confidence to become socially strong and economically aware

Hence, the significance of every contribution is multifold. The Tremendous spirit of volunteers and members helps Ekal in reaching even the remotest areas of rural India.

As we walk on a path to build a strong and educated nation, every individual, every effort and every minute counts.

CERTIFICATIONS

Circular No 7/2010 regarding validity of 80G Application

INCOME-TAX ACT

CIRCULAR

Section 10(23C)(iv) of the Income-tax Act, 1961 – Exemptions – Charitable or religious trusts/institutions

– Clarification regarding period of validity of approvals issued under section 10(23C)(iv), (v), (vi) or (via)

and section 80G(5) of the Income-tax Act.

Circular No. 7/2010 [F.No.197/21/2010-ITA-I], Dated 27-10-2010

1.The Board has received various references from the field formations as well as members of public about the

period of validity of approvals granted by the Chief Commissioners of Income Tax or Directors General of

Income Tax under sub-clauses (iv), (v), (vi) and (via) of Section 10(23C) and by the Commissioners of Income

Tax or Directors of Income Tax under Section 80G (5) of the Income Tax Act, 1961.

2. It has also been noticed by the Board that different field authorities are interpreting the provisions

relating to the period of validity of the above approvals in a different manner. The following instructions

are accordingly issued for the removal of doubts about the period of validity of various approvals

referred to above.

3. Sub-Clauses (iv) and (v) of Section 10(23C) were amended by Taxation Laws (Amendment) Act, 2006

by insertion of the following proviso to that clause:-

“Provided also that any (notification issued by the Central Government under sub-clause (iv) or subclause

(v), before the date on which the Taxation Laws (Amendment) Bill, 2006 receives the assent of

the President, shall at any one time, have effect for such assessment year or years, not exceeding three

assessment years) (including an assessment year or years commencing before the date on which such

notification is issued) as may be specified in the notification.”

The intention behind the insertion of the above proviso was laid out in the relevant portion of the

explanatory notes to the Taxation Laws Amendment Act, 2006 which reads as under:

“A need has been felt to dispense with the requirement of periodic renewal of notifications. The

requirement of periodic renewal of notifications has been resulting in delays in their renewal.

5.2 In order to overcome delays, the eighth proviso to section 10(23C) has been amended so as to

provide that the above mentioned limit of effectivity for three assessment years shall be applicable in

respect of notifications issued by the Central Government under sub-clause (iv) or sub-clause (v) before

the date on which Taxation Laws (Amendment) Bill, 2006 receives the assent of the President.

5.3 The Taxation Laws (Amendment) Bill, 2006 received the assent of the President on 13.07.2006.

Therefore, on account of the above amendment any notification issued by the Central Government

under the said sub-clause (iv) or sub-clause (v), on or after 13.07.2006 will be valid until withdrawn and

there will be no requirement on the part of the assessee to seek renewal of the same after three years.”

The intention of legislature that the approvals under Section 10(23C) (iv) & (v) after the cut off date

mentioned above would be a one time approval which would be valid until withdrawn, is thus

sufficiently clear.

4. Approvals under Sub-Clauses (vi) and (via) of Section 10(23C) are governed by the procedure

contained in Rule 2CA. Rule 2CA was amended w.e.f. 1.12.2006, inter alia by substitution of the existing

sub-rule 3 by a new provision which is reproduced below:-

“(3) The approval of the Central Board of Direct Taxes or Chief Commissioner or Director General, as the

case may be, granted before the 1st day of December, 2006 shall at any one time have effect for a period

of exceeding three assessment years.”

Read in isolation, without any further guidance as was given by way of explanatory notes to Finance

Act, 2006 in respect of amendment of sub-clauses (iv) & (v) of Section 10(23C), the above amendment

leaves some scope for doubt about the period of validity of the approval under Section 10(23C)(vi) and

(via) on or after 1.12.2006. For the removal of doubts if any in this regard, it is clarified that as in the

case of approvals under sub-clauses (iv) & (v) of Section 10(23C), any approval issued on or after

1.12.2006 under sub-clause (vi) or (via) of that sub-section would also be a one time approval which

would be valid till it is withdrawn.

5. As regards approvals granted upto 1.10.2009 under Section 80G by the Commissioners of Income Tax/

Directors of Income Tax, proviso to Section 80G(5) (vi) clarified that any approval shall have effect for such

assessment year or years not exceeding five assessment years as may be specified in the approval. The above

proviso was deleted by the Finance (No. 2) Act, 2009. The intent behind the deletion of above proviso as

explained in the explanatory memorandum to Finance (No.2) Bill, 2009 was as under:

“Further as per clause (vi) of sub-section (5) of section 80G of the Income-tax Act, 1961, the institutions

or funds to which the donations are made have to be approved by the Commissioner of Income-tax in

accordance with the rules prescribed in rule 11AA of the Income-tax Rule, 1962. The proviso to this

clause provides that any approval granted under this clause shall have effect for such assessment year

or years, not exceeding five assessment years, as may be specified in the approval.

Due to this limitation imposed on the validity of such approvals, the approved institutions or funds have

to bear the hardship of getting their approvals renewed from time to time. This is unduly burdensome

for the bona fideinstitutions or funds and also leads to wastage of time and resources of the tax

administration in renewing such approvals in a routine manner.

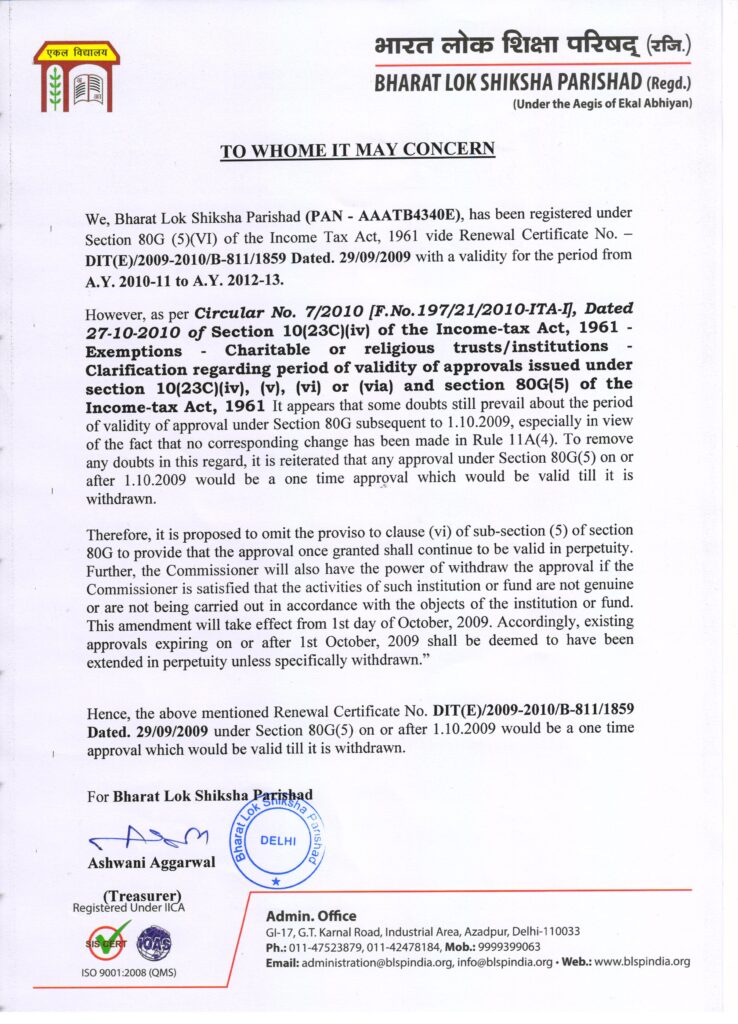

Therefore, it is proposed to omit the proviso to clause (vi) of sub-section (5) of section 80G to provide

that the approval once granted shall continue to be valid in perpetuity. Further, the Commissioner will

also have the power of withdraw the approval if the Commissioner is satisfied that the activities of such

institution or fund are not genuine or are not being carried out in accordance with the objects of the

institution or fund. This amendment will take effect from 1st day of October, 2009. Accordingly, existing

approvals expiring on or after 1st October, 2009 shall be deemed to have been extended in perpetuity

unless specifically withdrawn.”

It appears that some doubts still prevail about the period of validity of approval under Section 80G

subsequent to 1.10.2009, especially in view of the fact that no corresponding change has been made in

Rule 11A(4). To remove any doubts in this regard, it is reiterated that any approval under Section 80G(5)

on or after 1.10.2009 would be a one time approval which would be valid till it is withdrawn.